Hormuz at the Breaking Point, Why the New Sanctions Shock Could Reshape Energy, Power, and the Global Order

Oil above $109 is the headline. Control of fear, shipping, and strategic time is the deeper story.

SHADOWNET DESK | Novarapress Analysis

T

he world often notices the Strait of Hormuz only when oil spikes or warships move. That is a mistake. Hormuz is not merely a narrow waterway between Iran and the Arabian Peninsula. It is one of the central pressure valves of the modern global economy. When tension rises there, markets do not simply price barrels. They price uncertainty, insurance, military risk, diplomatic credibility, and the possibility that a regional confrontation could mutate into a global economic shock.

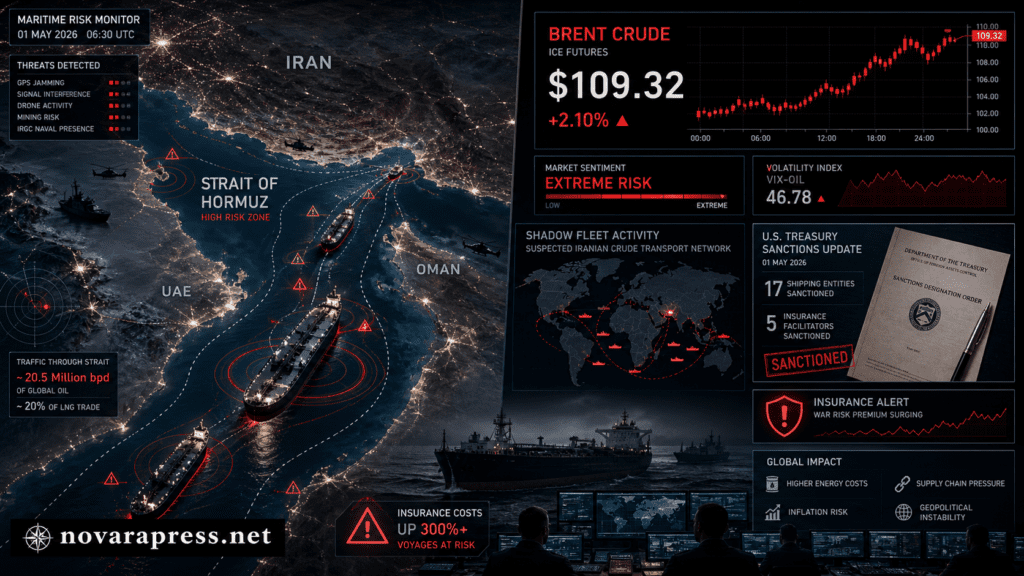

That is why the latest U.S. Treasury sanctions package matters far beyond the legal language of enforcement notices. By expanding secondary sanctions against shipping entities and insurance facilitators accused of helping covert Iranian exports, Washington has chosen to widen pressure not only on Tehran, but on the commercial ecosystem that keeps sanctioned oil moving. In response, Iran’s leadership has framed the move as siege warfare while leaving a narrow rhetorical door open to negotiations.

Brent crude crossing $109 per barrel is not the cause of this story. It is the symptom.

SECTION 01. The Real Battlefield Is Not the Water, It Is the System

Most observers imagine a Hormuz crisis as missile strikes, mines, drones, or naval escorts. Those remain real risks. But the immediate battlefield today is financial and logistical infrastructure.

Oil only reaches consumers through a chain of permissions:

- Ships willing to carry cargo.

- Insurers willing to cover voyages.

- Banks willing to process payments.

- Ports willing to receive cargo.

- Refiners willing to absorb legal risk.

Sanctions that target these nodes can choke trade without firing a shot. Washington understands this. Tehran understands it too. That is why both sides speak in military language while acting through commercial arteries.

The current sanctions wave suggests the United States believes Iran’s shadow export network has adapted too well to earlier restrictions. The answer now is not symbolic punishment. It is network disruption.

SECTION 02. Why $109 Matters More Than It Looks

Some readers will ask whether $109 oil is truly dramatic in historical terms. Prices have been higher before. But context matters.

Today’s world economy is more debt-heavy, more politically fragmented, and more inflation-sensitive than during previous oil shocks. That means a move above $109 can produce outsized psychological and policy consequences.

| Then | Now |

|---|---|

| Central banks tolerated inflation longer | Central banks fear inflation relapse |

| Supply chains less politicized | Supply chains already strained |

| Consumers less rate-sensitive | Households carry higher financing stress |

| Geopolitical blocs looser | Strategic blocs hardening |

So the same nominal price today can generate stronger economic tremors than in the past.

SECTION 03. Tehran’s Message Was Carefully Engineered

Iran’s leadership did not answer sanctions with a purely emotional speech. The language appears calibrated for three audiences at once.

Domestic audience: The state presents resilience, sovereignty, and endurance.

Regional audience: Iran signals it remains capable of shaping Gulf risk.

International audience: Phrases about “practical discussions” hint that pressure can still be converted into negotiation.

This is classic leverage politics. Iran wants to avoid appearing weak, avoid uncontrolled escalation, and preserve bargaining value simultaneously.

When a state cannot outmatch power directly, it often seeks to outprice it indirectly.

SECTION 04. America’s Calculation, Raise Costs Without Owning a War

Washington also faces constraints. The United States wants to limit Iranian revenue, reassure allies, and protect shipping lanes. But it likely prefers not to enter a major new regional war while managing multiple theaters and domestic political pressures.

That creates a familiar doctrine:

- Economic coercion over direct conflict.

- Maritime deterrence over invasion logic.

- Partner burden-sharing over unilateral policing.

- Incremental pressure over sudden shock.

The risk is that controlled pressure can still trigger uncontrolled responses. History repeatedly shows that actors under economic siege often search for asymmetric counters.

SECTION 05. The Shadow Fleet Problem

The sanctions focus on shipping entities and insurers points to a deeper phenomenon, the rise of the shadow fleet. These are aging vessels, opaque ownership structures, ship-to-ship transfers, flag changes, identity masking, and layered intermediaries used to move sanctioned crude.

This model has expanded because modern trade systems reward opacity when profits are high enough.

Destroying one network node rarely ends the trade. It often reroutes it. That means sanctions can succeed tactically while failing strategically if enforcement cannot adapt faster than evasion.

The present escalation suggests Washington believes adaptation remains possible.

SECTION 06. Who Feels Pain First

The immediate losers from a prolonged Hormuz premium are not necessarily the states exchanging threats. They are often importers with limited strategic depth.

Asia: India, Japan, South Korea, and China face elevated freight and feedstock risk.

Europe: Faces inflation spillover, industrial cost pressure, and competition for alternative fuels.

Emerging markets: Suffer currency weakness and subsidy stress.

Consumers: Higher transport costs can feed food prices and retail inflation.

In other words, a Gulf crisis becomes a tax on distance.

SECTION 07. Gulf Producers Gain and Worry at the Same Time

For major Gulf exporters outside Iran, higher prices can increase revenues. But the same crisis threatens the routes through which those revenues flow.

This creates a strategic paradox. Gulf states benefit from elevated prices but require stable corridors. Their likely preference is controlled firmness, not chaos.

Expect accelerated investment in:

- Pipeline bypass capacity.

- Red Sea and Arabian Sea export flexibility.

- Storage hubs abroad.

- Naval surveillance and drone defense.

- Strategic diplomacy with Washington, Beijing, and regional rivals.

SECTION 08. China’s Quiet Position

China may be one of the most important actors in this story while saying the least publicly. As a major importer with expanding global influence, Beijing dislikes both energy shocks and U.S.-dominated chokepoint politics.

China’s incentives likely include:

- Stable Gulf imports.

- Discounted sanctioned barrels when available.

- Avoiding direct confrontation.

- Long-term diversification through pipelines, renewables, and overseas assets.

If Hormuz instability persists, it strengthens China’s argument that the existing maritime order is too vulnerable to geopolitical weaponization.

SECTION 09. Why Insurance Markets Are the Hidden Trigger

Many crises focus on fleets and missiles. Professionals watch insurers. If underwriters sharply reprice risk or withdraw coverage, shipping can slow instantly even without combat.

This is because captains, charterers, and port authorities operate inside liability frameworks. No insurance can mean no voyage.

One of the fastest ways to create a supply shock is not sinking tankers. It is making them legally uninsurable.

SECTION 10. Three Scenarios from Here

Sanctions continue. Rhetoric stays high. Limited incidents occur. Oil ranges $105 to $115. This is the most probable near-term path.

A tanker seizure, strike, drone attack, or major insurance freeze pushes crude toward $120 to $130 rapidly.

Quiet mediation lowers enforcement friction. Prices retreat below $100 over time, but trust remains damaged.

SECTION 11. What the Market Is Really Asking

Markets are not asking whether Iran and the United States like each other. They are asking four harder questions:

- Can shipping remain routine?

- Can insurers price risk rationally?

- Can diplomacy contain accidents?

- Can spare supply cover panic?

As long as those answers remain uncertain, a premium stays embedded in every barrel.

SECTION 12. The Larger Historical Shift

For decades, globalization was built on the assumption that efficiency would outrun geopolitics. That era is fading. Strategic chokepoints are back. Shipping lanes matter again. Flags matter again. Energy security matters again.

Hormuz is therefore more than a regional flashpoint. It is a symbol of a world where commerce and coercion are re-merging.

States that built prosperity on cheap, uninterrupted flows now face a harsher truth. Supply chains are only as peaceful as the sea lanes beneath them.

Oil above $109 is not simply a commodity move. It is a vote of no confidence in strategic stability. The side that best manages time, nerves, and logistics, not slogans, will shape the next phase of the Hormuz contest.

Sources: Public sanctions announcements, energy market pricing, maritime risk frameworks, regional strategic assessments.