Energy Security / Strategic Risk

The 33-Mile Trigger: How the Strait of Hormuz Holds the Global Economy at Gunpoint

A waterway barely wider than a city is the single most consequential chokepoint in modern economic history. One closure scenario — even a partial one — would send fuel prices soaring within hours, fracture supply chains within weeks, and push entire economies into recession within months.

Find the Strait of Hormuz on any world map and you will be surprised by how small it looks. Wedged between the southern tip of Iran and the northern coast of Oman, this narrow passage connects the Persian Gulf to the Gulf of Oman and then to the wider Indian Ocean. At its narrowest navigable point, it is barely 33 miles across — roughly the distance from one side of a large metropolitan city to the other. Yet this unremarkable sliver of water is, in every meaningful economic sense, one of the most critical chokepoints on the planet. Close it, and the global economy does not slow down. It convulses.

Every single day, between 17 and 21 large oil tankers pass through the Strait of Hormuz, carrying an estimated 20 to 21 percent of the world’s total petroleum liquids — roughly 17 to 18 million barrels of crude oil, condensate, and refined petroleum products. Add to that approximately 4 billion cubic feet of liquefied natural gas (LNG) that moves through the strait daily, much of it destined for Asia and Europe, and you begin to understand the scale of what is at stake. This single passageway handles more energy cargo than any other chokepoint on earth, more than the Suez Canal, more than the Strait of Malacca, more than the Turkish Straits. No other piece of water carries this much economic weight per nautical mile.

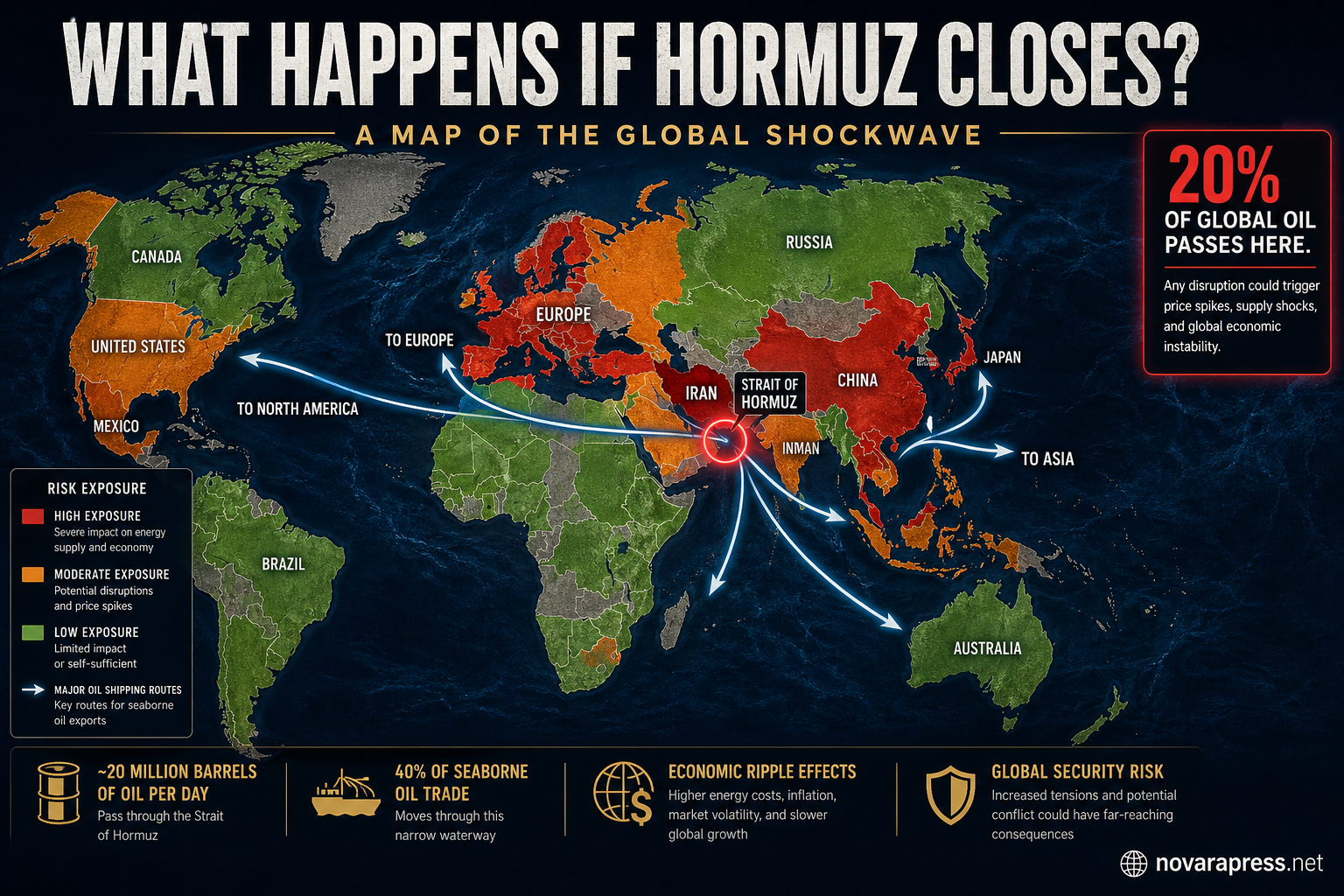

The nations that move their oil through Hormuz read like a list of the world’s largest producers: Saudi Arabia, Iraq, the United Arab Emirates, Kuwait, Qatar, and Iran itself all depend on the strait to reach export markets. For these Gulf states, there is no alternative that even comes close to the throughput capacity of Hormuz. Without it, their oil stays in the ground. Without it, the world’s largest consumers — China, Japan, South Korea, India, and the European Union — face sudden, catastrophic shortfalls. The math is straightforward. The implications are terrifying.

Why the World Built Its Energy System Around a Single Bottleneck

The dependence on the Strait of Hormuz was not an accident of planning. It was the outcome of decades of investment, infrastructure development, and geopolitical calculation across the Gulf region. When the major Gulf oil fields were developed in the mid-20th century, the fastest, cheapest, and most scalable method of moving crude to international markets was by sea. Pipelines existed, but they were expensive to build, slow to expand, and vulnerable to political complications crossing multiple national borders. Tankers, by contrast, could scale rapidly. Ports were built on the Gulf shore. Loading terminals were constructed. And the Strait of Hormuz, the only natural exit from the Persian Gulf to the open ocean, became the de facto artery of the global energy system.

Over the following decades, this dependence deepened as global demand for oil grew and as Gulf production capacity expanded dramatically. Saudi Arabia’s Ras Tanura terminal, the world’s largest offshore oil loading facility, sits squarely on the Persian Gulf side of Hormuz. The UAE’s major export terminals at Jebel Ali and Das Island feed directly into tankers that transit the strait. Qatar’s vast LNG export complex at Ras Laffan — the source of a significant share of the world’s LNG supply — depends entirely on Hormuz for its access to international markets. This infrastructure is not designed to pivot quickly. It was built specifically for this route, and it cannot simply be redirected overnight.

“The Strait of Hormuz is not merely a geographic feature. It is the single circuit breaker in the world’s energy grid — and right now, there is no backup switch.”

What makes Hormuz uniquely dangerous compared to other major chokepoints is the combination of three factors: volume, concentration, and irreplaceability. The Suez Canal carries significant cargo, but disruptions there can be partially mitigated by routing ships around the Cape of Good Hope — a longer and more expensive route, but a real one. The Strait of Malacca connects the Indian Ocean to the Pacific, but alternative routes through Indonesian waters exist. Hormuz has no true equivalent alternative for the volume of oil that passes through it. Any scenario that interrupts traffic at the strait does not redirect global oil flows. It eliminates them.

What Happens If Hormuz Closes

The closure of the Strait of Hormuz — even a temporary one lasting only a few days — would trigger a cascade of events that economists and energy analysts describe in terms usually reserved for natural disasters. It would begin almost immediately in the futures markets, long before the physical shortage reached consumer economies. Oil traders, responding to the news of any credible closure threat, would begin buying futures contracts to hedge against scarcity. Within the first 24 hours of a confirmed blockage, oil prices would likely surge by 30 to 50 percent. This is not speculation. Historical precedents from the 1973 Arab oil embargo, the 1979 Iranian Revolution, and Iraq’s invasion of Kuwait in 1990 all produced rapid, massive price spikes driven primarily by fear and market psychology, even before physical supply was materially disrupted.

If the closure persisted for one week, the picture would deteriorate significantly. Countries that maintain Strategic Petroleum Reserves (SPR) — the United States holds roughly 700 million barrels; the International Energy Agency member states maintain reserves equivalent to 90 days of net imports — would begin drawing down those stockpiles. But releases from SPRs are slow, administratively complex, and physically limited by the speed at which oil can be moved from storage to refineries. The psychological effect of watching reserves shrink would amplify the market panic rather than dampen it.

After one month of closure, the damage would transition from financial to structural. Refineries in Asia that run on Gulf crude would be forced to idle or switch to alternative feedstocks they are not designed to process efficiently. Petrochemical plants — the source of raw materials for plastics, fertilizers, pharmaceuticals, and industrial chemicals — would face input shortages that cascade down their entire supply chains. Airlines, already among the most fuel-sensitive industries, would begin canceling routes and grounding aircraft. Shipping costs across all commodities — not just oil — would spike, because a tighter oil market means tighter bunker fuel supply for cargo vessels, driving up the cost of moving everything from electronics to food.

Threat + 72 Hours

Markets surge 25–35%. SPR releases announced. Tankers rerouted to available alternatives. Temporary price pain, economic continuity maintained.

Closure 2–4 Weeks

Oil hits $140–$160/barrel. Refinery slowdowns in Asia. Inflation spikes globally. Recession risk elevated. Emergency energy summits convened.

Closure 3+ Months

Global recession. Fuel rationing in import-dependent nations. Political destabilization in energy-poor countries. Permanent supply chain restructuring begins.

The inflationary consequences of a sustained closure would reach far beyond the fuel pump. Oil is not simply a fuel. It is a feedstock for the global industrial system. Every ton of fertilizer used in modern agriculture depends on hydrocarbons. Every piece of plastic, every synthetic fiber, every pharmaceutical compound, every industrial lubricant traces its origins to petrochemical inputs. A sustained disruption to oil supply does not just raise gasoline prices. It raises the cost of producing food, medicine, clothing, electronics, and construction materials. In economies already running elevated inflation, a Hormuz closure would not add to the problem. It would transform it into a crisis of a different order entirely.

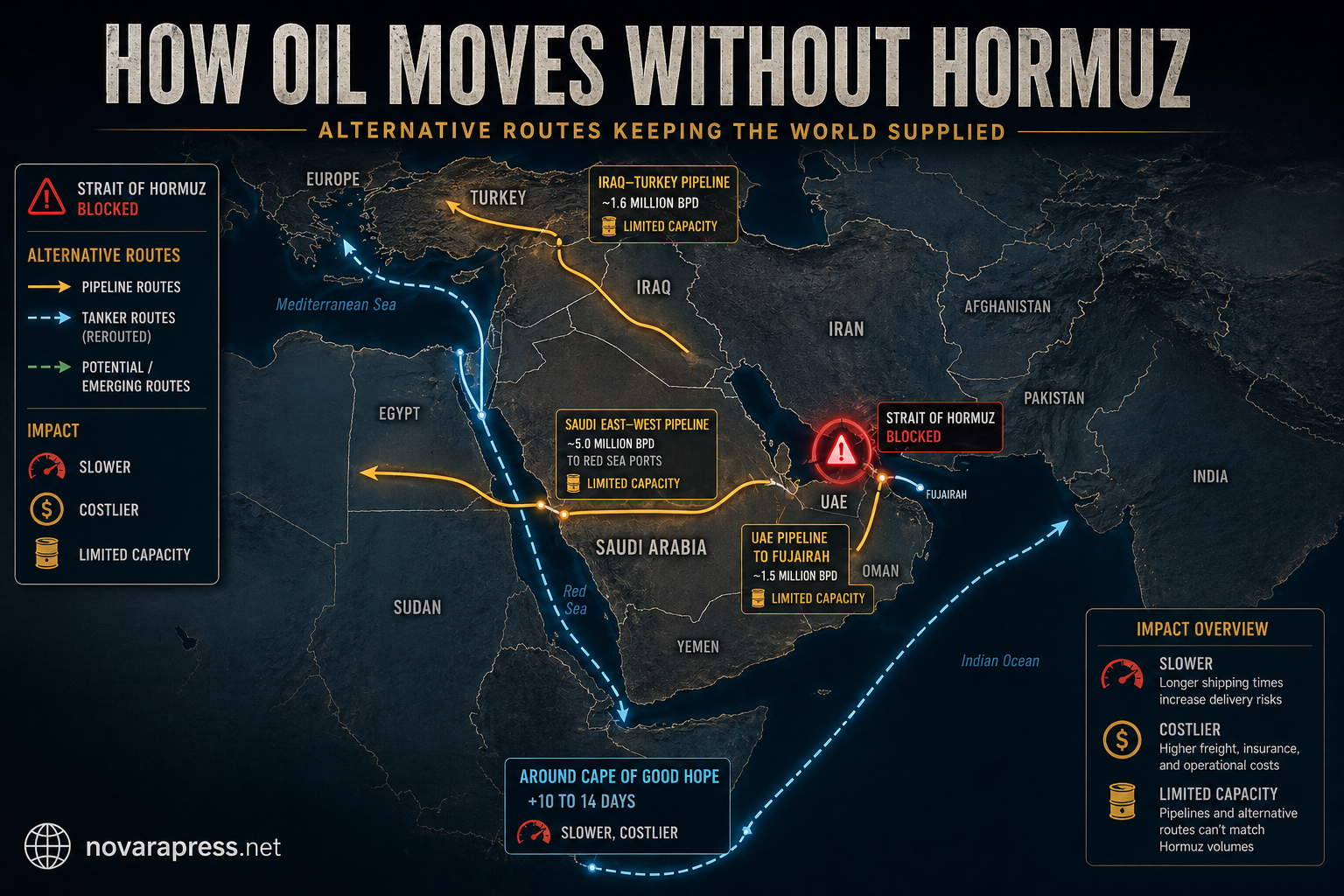

How Oil Moves Without Hormuz

The question that strategic planners and energy ministries across the Gulf have spent decades trying to answer is this: if Hormuz were closed, what alternatives exist? The honest answer is that alternatives exist, but none of them are adequate — not in terms of capacity, not in terms of speed, and not in terms of cost. The bypass infrastructure that exists today could handle, at maximum, a fraction of current Hormuz throughput. The rest of the world’s energy system would simply have to go without.

The most significant bypass option is the East-West crude oil pipeline in Saudi Arabia, also known as the Petroline. It runs approximately 1,200 kilometers from the Abqaiq processing facility in eastern Saudi Arabia to the Yanbu terminal on the Red Sea coast. The Petroline has a stated capacity of around 5 million barrels per day (mbpd), though current operating throughput is considerably lower. In a Hormuz closure scenario, Saudi Arabia could theoretically increase Petroline flows and export crude from Yanbu rather than from its Gulf terminals, bypassing the strait entirely. However, 5 mbpd is a fraction of the 17-18 mbpd that currently transits Hormuz. The Petroline does not solve the problem. It absorbs roughly a quarter of it at best.

| Bypass Route | Capacity (mbpd) | Operational Status | Covers Hormuz Gap |

|---|---|---|---|

| Saudi Petroline (East-West) | ~5.0 | Active (partial use) | ~28% |

| UAE Abu Dhabi Crude Oil Pipeline | ~1.8 | Active | ~10% |

| Iraq–Turkey Kirkuk Pipeline | ~0.9 | Partially disrupted | ~5% |

| Trans-Arabian Pipeline (Tapline) | — | Decommissioned | 0% |

| Cape of Good Hope Tanker Route | Unlimited | Active but +15 days | Delayed only |

The UAE completed its Abu Dhabi Crude Oil Pipeline (ADCOP) in 2012 precisely to reduce dependence on Hormuz. The pipeline connects the Habshan oil fields in the Abu Dhabi interior to the Fujairah terminal on the Gulf of Oman coast — outside the strait. Its capacity of approximately 1.8 mbpd gives the UAE a genuine, if limited, bypass option. Fujairah has grown into one of the world’s largest bunkering hubs partly because of its strategic position outside Hormuz. But 1.8 mbpd from the UAE, combined with Saudi Petroline flows, still leaves the world short by at least 10 million barrels per day. That is not a manageable gap. That is a structural emergency.

The Iraq–Turkey Kirkuk-Ceyhan pipeline offers another partial alternative, routing Iraqi crude northward through Turkey to the Mediterranean port of Ceyhan. But this pipeline has been plagued for years by operational disruptions, political disputes between Baghdad and Erbil, and technical damage. Its contribution to any Hormuz bypass would be uncertain at best, minimal at worst. The Trans-Arabian Pipeline that once carried Saudi crude to Lebanon’s Mediterranean coast has been decommissioned for decades and could not be restored to operation quickly under any realistic scenario.

The remaining option — routing tankers around the Cape of Good Hope rather than through Hormuz — is technically available but economically punishing and time-consuming. A tanker traveling from the Persian Gulf to Rotterdam via the Cape of Good Hope instead of via the Suez Canal adds roughly 15 to 20 days of sailing time. That extended voyage requires more fuel, more crew time, more wear on the vessel, and delays delivery schedules. In a market suddenly starved of supply, those additional two to three weeks of transit time would be catastrophic. The oil is still coming — but it arrives too slowly to prevent rationing, too expensively to avoid passing the cost on to consumers, and too uncertainly to stabilize the market panic.

“The alternatives to Hormuz are not solutions. They are pressure relief valves on a system designed to handle a fraction of the pressure.”

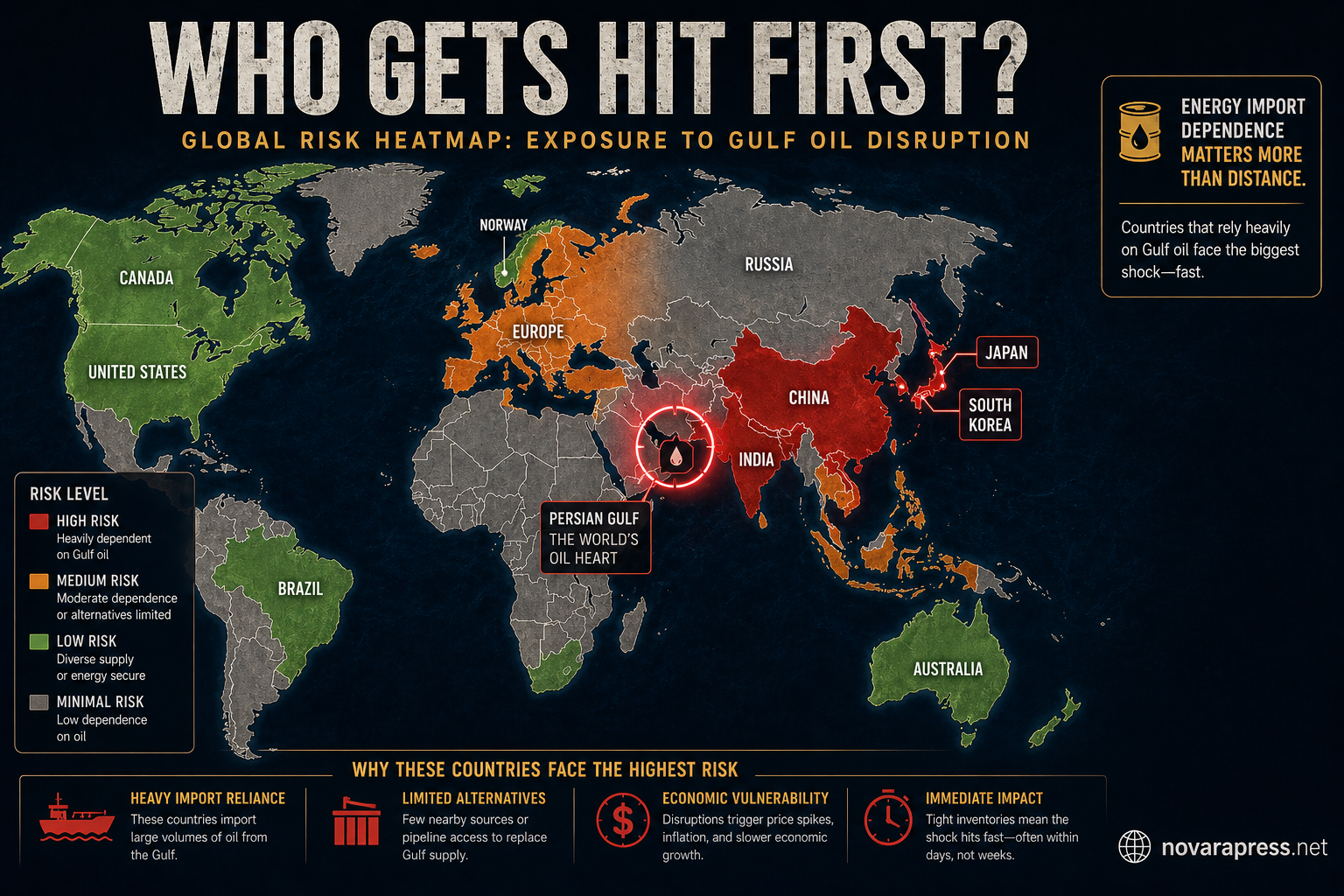

Who Gets Hit First

Not all countries are equally exposed to a Hormuz closure, but the pattern of vulnerability is stark and follows a clear geographic logic. The nations that depend most heavily on Gulf oil imports through the strait — and that have the fewest diversification options — will feel the impact fastest and most severely. Asia stands at the front of the line.

Japan imports approximately 90 percent of its crude oil from the Middle East, and the overwhelming majority of that supply transits the Strait of Hormuz. Japan has almost no domestic production, limited refining flexibility, and strategic reserves that could sustain the country for roughly 150 days of consumption. A closure lasting longer than that would not merely create economic hardship — it would force radical decisions about industrial production, heating, transportation, and food supply. Japan’s economy, the world’s third largest, would contract rapidly. South Korea faces an almost identical situation: near-total dependence on Middle Eastern crude, significant strategic reserves, but a petrochemical and manufacturing export economy that cannot function without oil inputs.

| Country | Gulf Oil Dependence | Hormuz % of Imports | SPR Coverage (days) | Vulnerability |

|---|---|---|---|---|

| Japan | ~90% | ~87% | ~150 | CRITICAL |

| South Korea | ~72% | ~70% | ~120 | CRITICAL |

| India | ~65% | ~60% | ~64 | HIGH |

| China | ~40% | ~38% | ~90 (est.) | HIGH |

| Germany / EU | ~30% | ~25% | ~90 | MODERATE-HIGH |

| United States | ~10% | ~8% | ~330 | MODERATE |

China is the world’s largest importer of crude oil and the single biggest buyer of Gulf crude. Approximately 40 percent of China’s total oil imports transit the Strait of Hormuz. Given that China imports roughly 11 million barrels per day, that represents nearly 4.5 million barrels daily that would be immediately disrupted by a closure. China’s strategic reserves, while substantial and not publicly disclosed in full, would face depletion pressure that no amount of domestic production increase could compensate for. A prolonged closure would force China to prioritize oil allocation between its manufacturing sector, its transportation infrastructure, and its strategic military requirements — a set of choices that would have profound implications for global supply chains already under strain.

India presents a particularly vulnerable profile. Heavily dependent on Gulf crude imports, India has less developed strategic reserve infrastructure than Japan, South Korea, or China. Its reserves cover only around 60 to 65 days of consumption. India’s rapid industrial growth and expanding middle class have made it the world’s third-largest consumer of crude oil, but its domestic production covers less than 20 percent of its needs. A Hormuz closure would hit India’s economy at precisely its most exposed point: fuel costs for agriculture and transportation — sectors that directly determine food prices for more than a billion people.

Europe’s exposure is significant but somewhat more buffered than Asia’s. European nations have more diversified energy relationships — North Sea production, Norwegian gas, Algerian pipeline supplies, Libyan crude, and in the medium-term, North American LNG exports — that reduce but do not eliminate the continent’s dependence on Hormuz-transiting energy. Germany, France, Italy, and Spain import meaningful volumes of Gulf crude, and Europe collectively takes significant quantities of Qatari LNG that moves through the strait. A closure would raise European energy costs sharply, reignite inflationary pressures that central banks have spent two years trying to suppress, and create political tensions within the EU over energy burden-sharing.

The United States occupies a comparatively privileged position. The shale revolution transformed America into the world’s largest oil producer, and the country now imports relatively little from the Gulf. However, the U.S. economy remains embedded in global markets where oil is priced internationally. When Brent crude spikes by 40 percent, gasoline prices in Kansas rise almost as fast as gasoline prices in Seoul. The dollar-denominated nature of global oil trade means that no economy, however domestically energy-sufficient, is truly insulated from a Hormuz shock.

How Governments and Markets Have Prepared — and Why It Is Not Enough

The international community has not been unaware of the Hormuz risk. Since the tanker wars of the 1980s — when Iran and Iraq attacked each other’s oil shipping during their eight-year war — governments have invested in both military and economic infrastructure designed to manage closure scenarios. The U.S. Fifth Fleet is based in Bahrain specifically to ensure freedom of navigation through the strait. NATO and regional naval forces conduct regular escort operations and exercises designed to protect tanker traffic. These military deterrents have succeeded in preventing full closure so far, but they cannot guarantee that no closure ever occurs, and they cannot substitute for energy supply if the strait is genuinely blocked.

The International Energy Agency (IEA) coordinates among its 31 member nations to maintain strategic petroleum reserves sufficient to cover 90 days of net oil imports. In a supply emergency, the IEA can authorize coordinated SPR releases to flood the market with stored oil, dampening the price spike and buying time for diplomatic or military resolution of the crisis. This mechanism was used during the 1991 Gulf War and again during the 2011 Libyan civil war. It provides a meaningful short-term buffer. But 90 days is a finite window. If a Hormuz closure lasted beyond three months, the IEA mechanism would be exhausted, and the world would face a structural supply deficit with no reserve cushion remaining.

“Strategic reserves exist to buy time for diplomacy or war to restore supply. They are not a substitute for supply. They are a countdown clock.”

The financial markets have developed their own Hormuz-risk mechanisms. Energy futures markets allow oil consumers — airlines, shipping companies, utilities, industrial producers — to hedge against price spikes through forward contracts and options. These instruments do not prevent prices from rising. They transfer the cost of rising prices from one party to another. For the broader economy, hedging spreads the pain rather than eliminating it, and for small businesses and consumers who cannot access futures markets, no hedge exists. They simply pay more.

Several Gulf states have invested in bypass infrastructure as part of their long-term strategic planning. Saudi Arabia has expanded Petroline capacity and worked to increase Yanbu’s export capabilities. The UAE has maximized the utility of its Fujairah pipeline and terminal complex. Qatar has explored LNG routing options that reduce Hormuz dependence. But none of these investments has come close to creating a genuine alternative that could substitute for Hormuz at scale. The economics of pipeline construction and the geography of the Gulf region make full bypass capability essentially impossible to achieve within any realistic timeframe or budget.

This Is Not a Middle East Story — It Is a Cost of Living Story

The most persistent misunderstanding about the Strait of Hormuz is that it is primarily a Middle Eastern problem — a regional geopolitical tension that affects oil-producing states and their immediate neighbors. This framing is wrong. The Hormuz question is ultimately a question about the cost of food in Nigeria, the price of electricity in Poland, the inflation rate in Brazil, and the purchasing power of working families in South Korea and Germany and Canada. It is, above all, a story about how a 33-mile passage of water has become the stress point for the entire global economic system.

Modern supply chains depend on affordable, predictable energy costs at every stage of production. A factory in Vietnam that assembles electronics for export to Europe depends on oil for its raw plastic materials, for the fuel that powers its logistics trucks, for the bunker fuel that moves its container ships across the Pacific. A wheat farm in Ukraine depends on diesel for its tractors and on natural gas-derived fertilizer for its soil. A grocery store in Mexico depends on refrigerated transport that runs on fuel. When oil prices spike — regardless of whether the cause is a war, an embargo, or a Hormuz closure — this chain of dependencies translates into higher costs at every link, and those costs ultimately land on the consumer who can least afford to absorb them.

The populations most vulnerable to a Hormuz-driven inflation shock are not in the wealthy oil-importing nations of Western Europe or East Asia, where economies have buffers, social safety nets, and central banks with tools to manage inflation. The most vulnerable populations are in lower-income import-dependent countries — Bangladesh, Pakistan, Egypt, Ethiopia, many sub-Saharan African nations — where fuel and food costs represent a large share of household expenditure, where currencies have limited defense against dollar-denominated energy price shocks, and where governments have neither the fiscal capacity to subsidize relief nor the strategic reserves to buffer the initial blow.

A Hormuz closure in the modern era would be an event whose immediate military and geopolitical dimensions would dominate headlines, but whose most lasting damage would be measured in hunger, unemployment, political destabilization, and generational poverty across dozens of countries that have no party to the conflict and no seat at the negotiating table. That is the true weight of 33 miles of water. That is what makes the Strait of Hormuz not merely a strategic concern for energy ministries and naval planners, but a moral and civilizational question for the entire global order.

The Strait of Hormuz remains the single most consequential geographic vulnerability in the global economic system. Despite decades of investment in bypass infrastructure, strategic reserves, and military deterrence, no adequate redundancy has been built. The strait’s closure — even partial, even temporary — would produce economic shockwaves that reach every corner of the world within days. The architecture of the global energy system was built around this bottleneck. Dismantling that dependence is a project measured in decades and trillions of dollars. Until that project is complete, 33 miles of water in the Persian Gulf carry the weight of the world economy on their surface every single day.

// Sources //

- U.S. Energy Information Administration (EIA) — World Oil Transit Chokepoints, 2024 Update

- International Energy Agency (IEA) — Oil Supply Security: Emergency Response of IEA Countries

- Oxford Institute for Energy Studies — Hormuz Closure Scenarios and Bypass Options (2023)

- Saudi Aramco — East-West Pipeline Technical Specifications and Capacity Reports

- ADNOC — Abu Dhabi Crude Oil Pipeline (ADCOP) operational data, Fujairah Terminal

- IMF World Economic Outlook — Oil Price Shock Transmission Mechanisms (2024)

- Congressional Research Service — Strait of Hormuz: Background and Issues for Congress

- Reuters / Bloomberg Energy Desks — Hormuz traffic monitoring and tanker tracking, 2024–2026