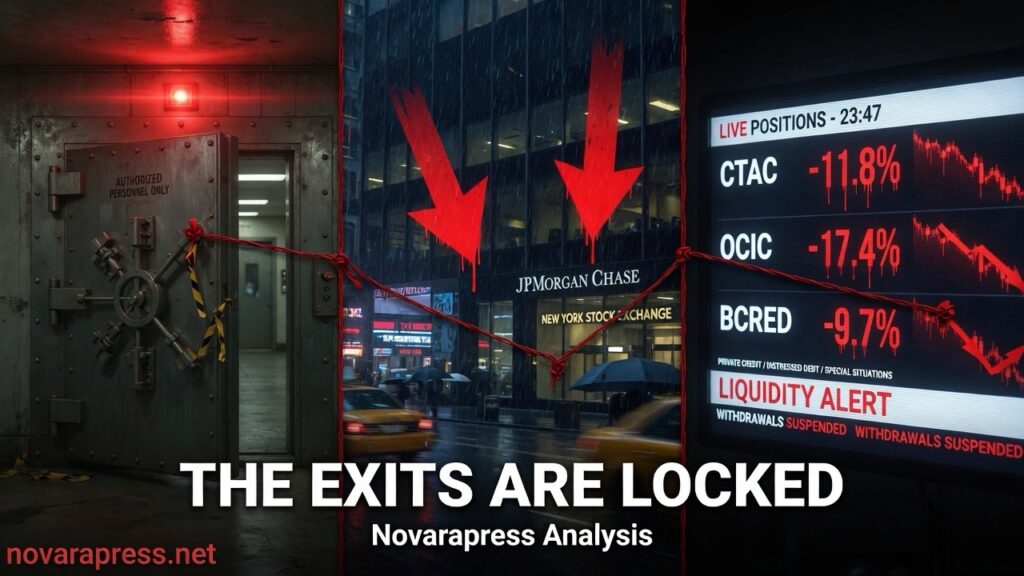

The Exits Are Locked: Inside the $20 Billion Run on Private Credit

In the first quarter of 2026, investors asked to pull $20.8 billion from private credit funds managed by some of Wall Street’s biggest names. They got back less than a third of it. The rest is still locked inside funds that were sold to retail investors as “semi-liquid” — a term that, under stress, turns out to mean something closer to “illiquid unless we decide otherwise.”

This is not a minor technical adjustment. It is the first serious stress test of a $3.5 trillion industry that spent a decade expanding into retail wealth management on the promise of bond-like accessibility with private equity-like returns. The promise is now visibly breaking down.

The Numbers Nobody Is Saying Out Loud

Start with Carlyle. Its Tactical Private Credit Fund, a $7 billion vehicle, received redemption requests totaling 15.7% of assets in Q1 — more than three times its 5% quarterly limit. Investors asked to withdraw roughly $750 million. They received approximately $240 million. The remaining $510 million stays locked in.

Blue Owl is worse. Its $36 billion Credit Income Corp fund saw 21.9% redemption requests. Its technology-focused fund — a $6.2 billion vehicle with heavy exposure to software companies — saw investors attempt to withdraw 40.7% of shares in a single quarter. Both figures rank among the highest quarterly redemption requests the industry has ever recorded. Blue Owl honored 5% of each.

The pattern holds across the industry. Apollo received 11.2% redemption requests. Ares hit 11.6%. Blackstone’s flagship private credit fund saw a record 7.9% — roughly $3.8 billion — and chose to honor the full amount rather than gate, a decision that is itself a signal of how badly the industry needs to avoid headlines. In February 2026, Blue Owl permanently froze redemptions in its Capital Corporation II fund, converting it from a semi-liquid vehicle into a drawdown structure where capital returns on the manager’s schedule, not the investor’s.

What “Semi-Liquid” Actually Means

Private credit funds are not banks. They do not hold Treasury bills or publicly traded bonds that can be sold in minutes to meet a wave of withdrawal requests. They hold loans to private companies — leveraged buyouts, software firms, middle-market businesses — that cannot be liquidated quickly without accepting distressed prices. Quarterly redemption windows of 5% were designed to manage the mismatch between portfolio illiquidity and investor expectations. The design works when a small fraction of investors want out at any given time. It fails when a large fraction decides to leave simultaneously.

That is what happened in Q1 2026. The triggers are not hard to identify: a war that disrupted global energy supply chains, rising inflation, AI-related fears about software loan portfolios, and a handful of high-profile fund-level blowups including First Brands and Tricolor. When BlackRock’s TCP Capital reported in Q4 2025 that writedowns had reduced its net asset value by 19%, the message reached every retail investor who had been told private credit was a stable income product.

What these investors are now discovering is that the 5% redemption cap — described by Blackstone’s Jon Gray as “a feature, not a bug” — means that in a genuine run, they could be locked out for years. If redemption requests stay elevated for multiple consecutive quarters and funds honor only 5% each time, an investor seeking full redemption at 15% quarterly demand faces a wait measured not in weeks but in years.

The Deeper Problem

To meet redemption requests, funds have two options: sell assets or borrow against credit lines. Both carry costs that fall on the investors who stay. Selling assets under pressure means selling the most liquid holdings first — which means the remaining portfolio becomes progressively less liquid and, potentially, lower quality. Borrowing to fund redemptions adds leverage to a fund already under stress.

The $20.8 billion in Q1 redemption requests represents roughly 7% of the approximately $300 billion in retail-accessible private credit assets tracked by the Financial Times. That is a large number for one quarter. Moody’s has already issued a negative outlook on the sector. The question being asked quietly in fund boardrooms is not whether this wave passes — it is whether the next wave is larger.

Private credit grew from a niche institutional product to a $3.5 trillion industry in roughly a decade, largely by convincing pension funds, endowments, and ultimately retail investors that it offered a better risk-adjusted return than public bonds. That argument depended on the assumption that exit options, while limited, were real. The events of Q1 2026 have demonstrated that when enough investors test that assumption at once, the exits lock.

The money is still in the funds. The question is when — and at what price — investors will get it back.