France Pulled Its Gold From America. Here’s What That Really Means.

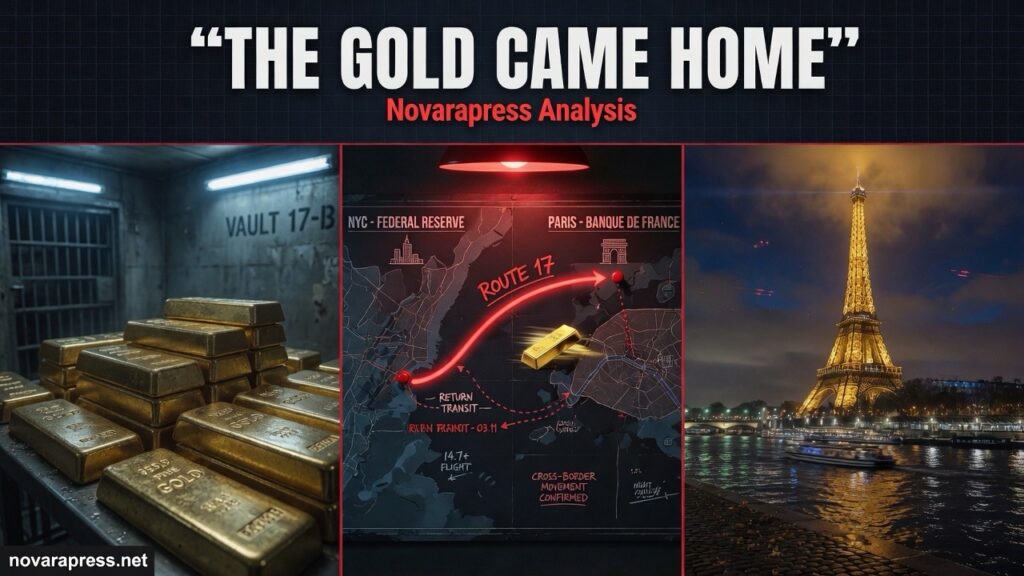

It didn’t make front-page headlines. There were no press conferences, no dramatic announcements, no diplomatic incidents. Between July 2025 and January 2026, the Banque de France quietly sold 129 tonnes of gold stored in the vaults of the Federal Reserve Bank of New York — and bought an equivalent amount of new, higher-standard bullion in Europe. The entire operation netted nearly $15 billion in profit.

France’s 2,437 tonnes of gold reserves are now held entirely in Paris. For the first time in roughly a century, not a single French bar sits beneath the streets of Lower Manhattan.

The official explanation is technical. The bars in New York were old — some dating back to the late 1920s — and no longer met modern international purity and weight standards. Shipping them across the Atlantic would have been expensive and logistically complex. Selling in New York and buying fresh bullion in Europe was simply cleaner. The Bank of France’s governor, François Villeroy de Galhau, was explicit: the decision was “not politically motivated.”

Maybe. But the timing tells a different story.

The Context That Changes Everything

This transaction was completed in January 2026 — weeks before the United States and Israel launched military operations against Iran, triggering the closure of the Strait of Hormuz, the worst energy supply shock in the history of the oil market, and a global economic slowdown that the IMF is now scrambling to quantify.

It came after years of escalating friction between Washington and its European allies — over tariffs, over NATO burden-sharing, over Ukraine, over the freezing of Russian central bank assets following the 2022 invasion, which sent a quiet but unmistakable signal to every finance ministry on earth: assets stored under American jurisdiction are not beyond American reach.

And it came as central banks worldwide have been stockpiling gold at a pace not seen since the Cold War — a trend driven not by nostalgia for the gold standard, but by a calculated desire to hold something that no government can freeze, sanction, or print away.

The Banque de France can call it a technical upgrade. The rest of the world is reading it as something else.

What France Actually Did — And What It Didn’t

Precision matters here. France did not physically transport gold bars across the Atlantic. It sold the old New York stock at peak market prices — gold was trading near historic highs in late 2025 — and used the proceeds to purchase new, LBMA-compliant bars in Europe. The total volume of France’s reserves remained unchanged. The profit came from the price differential between selling high in New York and buying at slightly lower rates in the European market.

The operation was executed across 26 separate transactions, a deliberate approach that avoided flooding the market and minimized price impact. It was methodical, professional, and — until recently — almost entirely under the radar.

What changed is that the world found out. And the world is now asking: if France is doing this, who else is considering it?

France Was Not the First. It Won’t Be the Last.

Germany completed a similar repatriation between 2013 and 2017, moving 674 tonnes of gold from New York and Paris back to Frankfurt. The process took four years and was initially met with quiet resistance before eventually being accommodated. The Netherlands repatriated 122 tonnes from New York in 2014. Hungary, Poland, and several other Central and Eastern European nations have since moved to consolidate their gold holdings domestically.

The pattern is consistent: countries that once trusted the United States as the natural custodian of their most valuable strategic reserves are quietly, methodically, bringing those reserves home.

Italy holds roughly 43 percent of its gold in the United States. Germany still keeps a significant share in New York. If the France move accelerates the conversation in Rome or Berlin, the geopolitical implications dwarf the $15 billion France just pocketed.

The Russian Asset Precedent

To understand why this matters, you need to understand what happened to Russian central bank assets in February 2022.

When Russia invaded Ukraine, the United States and its allies froze approximately $300 billion in Russian sovereign assets held in Western financial institutions. It was an unprecedented move — the largest seizure of a sovereign nation’s foreign reserves in modern history. The legal basis was contested. The precedent was undeniable.

Every finance ministry and central bank in the world took note. The implicit assumption that had underpinned the postwar financial order — that sovereign assets stored in allied countries were safe regardless of political circumstances — had been shattered. If it could happen to Russia, the logic goes, under the right conditions, it could happen to anyone.

France’s decision to complete its gold repatriation in this environment is not a coincidence. It is a hedge. A quiet, profitable, technically defensible hedge — but a hedge nonetheless.

What the Numbers Say About Trust

The Federal Reserve Bank of New York’s vault, located 80 feet below street level in Lower Manhattan, is believed to hold approximately 6,000 tonnes of gold on behalf of around 36 foreign governments and central banks. It has been the world’s most important gold custodian for the better part of a century — a role built on the assumption that the United States was the most stable, most reliable, most untouchable place to store a nation’s most critical financial asset.

That assumption is being tested. Not shattered — but tested.

Central banks globally have been diversifying away from dollar-linked assets for years. The dollar’s share of global foreign exchange reserves has declined steadily. Gold purchases by central banks hit multi-decade highs in 2022 and 2023, and remained elevated through 2025. The Iran war, the Hormuz closure, and the cascading economic disruptions of early 2026 have only accelerated a trend already well underway.

France’s move fits this pattern precisely. It is one data point in a longer arc — but it is a significant one, because France is not a peripheral economy hedging against instability. It is the world’s seventh-largest economy, a founding member of NATO, America’s oldest ally, and the holder of the fourth-largest gold reserves on earth.

The Macron Factor

Emmanuel Macron has spent much of his presidency articulating a doctrine of European strategic autonomy — the idea that Europe must reduce its structural dependence on the United States across defense, technology, energy, and finance. It is a position that has put him at odds with Washington repeatedly, and one that has gained considerably more traction in European capitals since the return of Donald Trump to the White House.

Whether or not Macron personally drove the gold decision — and the evidence suggests the Banque de France operated independently, as central banks are designed to do — the optics are inseparable from his broader political project. A France that keeps its gold in Paris is a France that is practicing what its president preaches.

American officials have publicly downplayed the move, characterizing it as routine portfolio management. Privately, the signal is harder to dismiss. When your oldest ally decides it no longer wants its most valuable strategic asset stored on your soil, the message transcends central banking.

The Honest Assessment

The more dramatic interpretations of this story — that Macron is declaring financial war on America, that France is preparing for dollar collapse, that Trump is about to seize foreign gold reserves — go well beyond what the evidence supports. The Banque de France is a professionally managed institution that made a financially rational decision at a favorable moment in the gold market. The profit alone justifies the transaction on purely technical grounds.

But financial decisions do not happen in a vacuum. They happen in a world where the freezing of Russian assets demonstrated that “safe” is a political judgment, not an absolute condition. They happen in a world where the Strait of Hormuz is effectively closed, where the dollar’s dominance is being tested from multiple directions simultaneously, and where central banks are quietly treating gold not as a relic of a past monetary system, but as the one asset that sits outside the reach of any single government’s decisions.

France moved its gold home. It made $15 billion doing it. And it sent a message that no official statement will officially acknowledge — but that every finance ministry in the world just received.

The Question That Follows

Who is next?

Italy holds a substantial share of its reserves in the United States. So does Japan. So does South Korea. If the conversation in those capitals shifts from “should we?” to “when should we?”, the implications for the dollar’s role as the world’s reserve currency anchor extend far beyond any single gold transaction.

France did not fire a shot. It sold some old gold bars, bought new ones closer to home, and booked a tidy profit. But in geopolitics, the quietest moves are often the ones that matter most.

The vaults beneath Manhattan are still full. For now.